Over the past two years, something unusual happened in venture capital.

Seven top-tier funds published theses on the same opportunity. Not adjacent ideas. The same idea. Index Ventures, Emergence, OpenOcean, Bessemer, a16z, Y Combinator, and Sequoia all independently arrived at the same conclusion.

The next wave of venture-backed companies will not sell software to service firms. They will be the service firm.

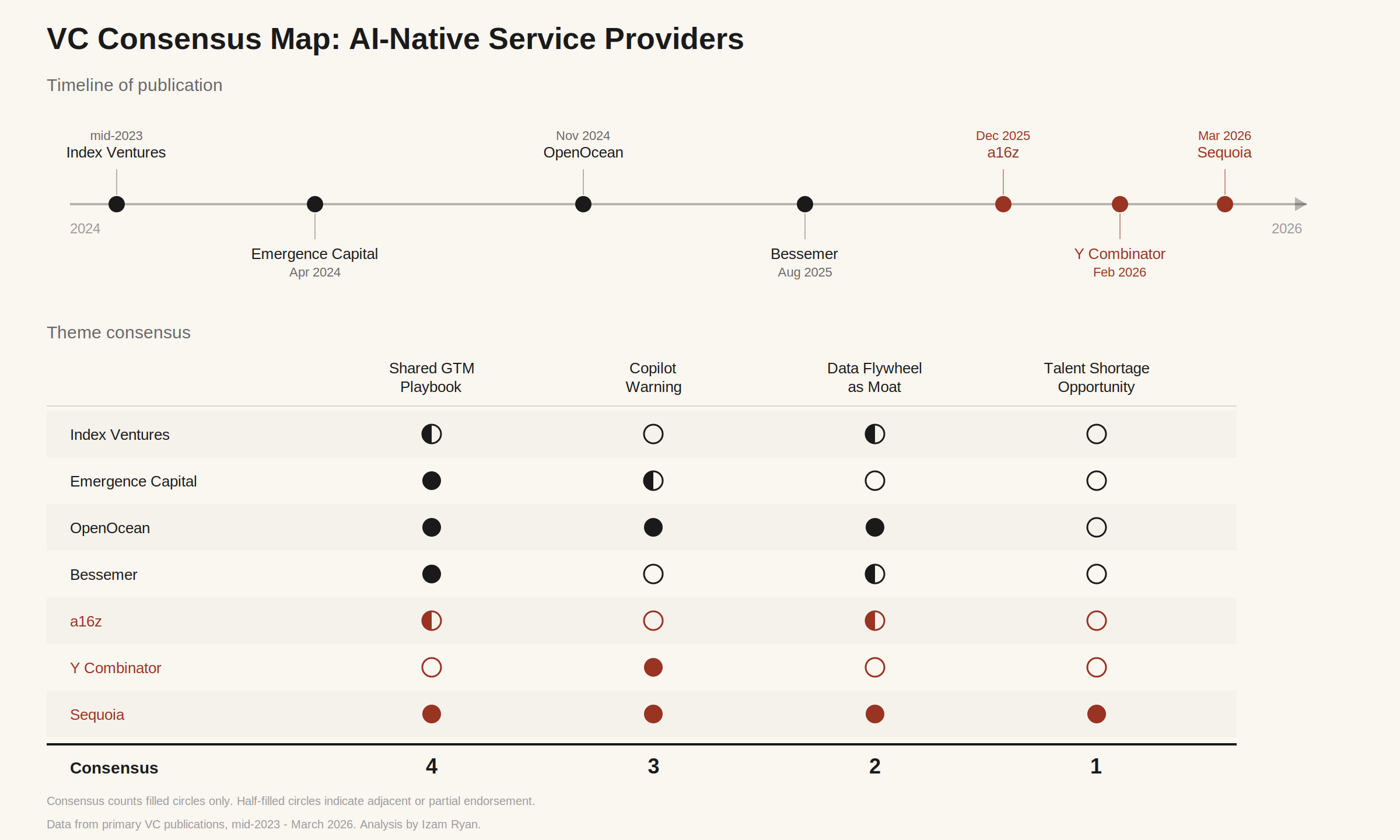

Seven top-tier VC funds published theses on AI-native service providers between mid-2023 and March 2026. Three of the biggest names landed in a single quarter. The consensus grid maps each fund’s thesis against four recurring themes, based on primary source analysis of each fund’s published work.

From contrarian to consensus in two years

Index Ventures was arguably first, arguing as early as 2023 that the next iteration of vertical SaaS would be vertically-focused AI platforms built on industry-specific datasets. Emergence Capital followed in April 2024 with “The Death of Deloitte,” arguing that AI-native services businesses could challenge the Big 4’s $200 billion revenue base. At the time, it still read as contrarian. Then the thesis started spreading.

OpenOcean published their AI-enabled services thesis in late 2024, arguing that the best opportunities sit in large, fragmented markets with repetitive, human-intensive work under cost pressure. Bessemer’s “Future of AI is Vertical” series followed in August 2025, reporting vertical AI companies growing at 400% year-over-year with margins that match traditional SaaS.

Then in Q1 2026, three of the biggest names in venture landed in a single quarter. a16z’s Big Ideas 2026 named finance and accounting as the next vertical AI breakout. Y Combinator’s Spring 2026 Request for Startups made AI-native agencies an explicit category, arguing these companies can achieve 65 to 80% gross margins. And Sequoia published “Services: The New Software” in March 2026.

The framing is blunt: for every dollar spent on software, six dollars are spent on services. VCs spent two decades funding the one-dollar market. The six-dollar market is next.

No VC thesis in recent memory has moved from contrarian to consensus this fast.

The copilot warning is the sharpest signal

Across these theses, four themes recur. A shared go-to-market playbook. The copilot warning. The data flywheel as a competitive moat and the talent shortage as a structural driver.

The copilot warning is the one that matters most.

Sequoia draws a clean line. A copilot sells the tool. An autopilot sells the work. The copilot makes a human more productive.

The autopilot delivers the finished outcome. When the underlying model improves, the copilot’s product gets thinner because the same acceleration is available to everyone. The autopilot’s margins get better because every improvement makes its service faster, cheaper, and harder to replicate.

OpenOcean arrives at the same conclusion from a different direction: “You move from selling the shovel to mining the gold.” Y Combinator frames it through economics: the value is not in the tool, it is in the result. Three of the seven funds I reviewed converge on this warning, independently and in different language.

This is not a technology distinction. It is a business model distinction with structural consequences for every professional services firm in the market.

The flywheel only compounds when the work is re-engineered

What the VC consensus identifies is real. What it lacks is a diagnostic.

The theses describe a shift from tools to outcomes. Several funds gesture toward proprietary data as a competitive advantage. But they do not distinguish between the companies that will actually build compounding flywheels and the ones that will hit a ceiling, despite raising significant capital on the same thesis.

Only two of the seven, Sequoia and OpenOcean, describe the compounding mechanism explicitly. The rest of the consensus has not yet articulated why some of these bets will compound and others will stall. That gap is what this analysis addresses.

Alexandra Najdanovic’s AI Classification framework at Aieutics provides the missing diagnostic. She identifies three classes of AI initiative, defined not by what the technology does, but by what the organisation would have to undo if the AI were removed.

Optimisation improves an existing process within the current operating model. Same people, same decisions, faster output. If you removed the AI tomorrow, the organisation reverts to its previous state. Fully reversible.

Transformation changes how the organisation operates. New roles, new structures, new ways of working. Reverting is unthinkable because the business has fundamentally reorganised around the capability. Irreversible.

Apply this to the consensus map. The copilot companies are optimisation. They accelerate existing workflows. The accountant still does the same job, faster.

The data from engagement number 100 is structurally identical to engagement number one. There is nothing new for the system to learn from. The flywheel does not compound because nothing has been re-engineered.

The autopilot companies are transformation. The work itself changes. The accountant shifts from preparer to validator. The client’s data estate is restructured for machine consumption.

Each engagement deepens the system’s understanding of entity mappings, extraction patterns, and financial taxonomies. The flywheel compounds because the architecture captures structural knowledge, not just speed.

This is the 80/20 flip in practice. Finance teams have historically spent 80% of their time on production work and 20% on strategy. When the production layer is automated and reliable, the ratio inverts. But “reliable” is the operative word.

In accounting, in legal, in audit, the output has to be right every time. Not almost always right. Right. That is a deterministic constraint, and generic AI is probabilistic.

In a due diligence engagement, when the question is “what was LTM EBITDA?”, the system needs to return the same number whether it is asked once or a thousand times. The architecture that solves this is what separates the autopilots that scale from those that produce impressive demos and then fail the first audit.

The gap the capital has not priced in

There are two layers the VC theses do not reach. The first is labour supply.

Sequoia’s thesis cites a figure worth sitting with. The US has lost roughly 340,000 accountants over five years. 75% of CPAs are nearing retirement. The licensing path is long and starting salaries lag technology and finance.

Most commentary frames AI-native services as disruption. The reality is different. In accounting, there will not be enough humans to do the work regardless of whether AI arrives. The question is not whether AI takes these jobs but who fills the gap when the workforce disappears.

The second layer is data readiness. Every autopilot thesis assumes the data is ready for AI to ingest. It is not.

Most small and mid-market business bookkeeping was designed for humans to read. Timesheets typed into free-text fields. Cost data in email threads. Revenue recognition logic that exists in someone’s head.

The information is there. It was never designed to be machine-readable. Structuring that data for AI consumption is the implementation gap between VC thesis and operating reality.

Without it, the autopilots have nothing to ingest. The flywheel has nothing to compound. The billions in committed capital are pointed at a market where the foundational data layer is still being built.

Where this leaves the firms that matter

The consensus points in one direction. The ventures this capital is flowing toward are not building tools for today’s firms. They are building the firms themselves.

The ones doing it well share a pattern. They started with deep domain knowledge, the kind that takes years in the room to accumulate. They re-engineered where they sit as an inescapable part of the value chain, not at the periphery where substitution is easy. And they built sticky data flywheels that compound the benefit of proprietary data on human-led decisions into training sets for the autopilots of tomorrow.

That stickiness is the point. Copilots face a structural ceiling because every improvement in the general-purpose models narrows their advantage. The accountant using a copilot today will be using a better, cheaper one next year from a different vendor. The autopilot that restructured the client’s data estate, retrained its extraction models on thousands of entity mappings, and embedded itself into the decision workflow has built something that does not commoditise with the next model release.

The capital knows where it is going. The question is whether the firms that should be building this, the ones with the domain knowledge, the client relationships, and the institutional memory, will re-engineer before the window closes.