The question keeps surfacing in boardrooms and product strategy meetings alike: should a business build its own payment infrastructure from the ground up, or leverage a white-label solution and focus resources on growth? It sounds like a classic build-vs-buy debate, but in the payments space, the stakes — financial, operational, and competitive — are considerably higher than in most software decisions. As the global payments landscape grows more complex, the answer is becoming harder to dodge.

The Real Cost of Going In-House

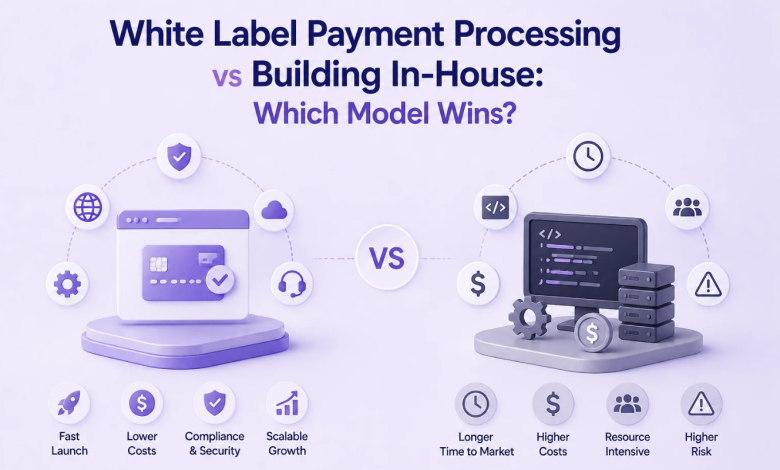

On the surface, building proprietary payment infrastructure has an undeniable appeal. Full control over the stack, custom logic tailored to your exact needs, no third-party dependencies. For large enterprises with deep engineering talent and regulatory expertise, it can even make strategic sense. But for the overwhelming majority of businesses, the numbers are brutal.

Developing a bespoke payment gateway from scratch costs anywhere from $250,000 to over $1 million, depending on the complexity of features, compliance certifications — most notably PCI DSS — and the depth of the acquirer network required. That’s before accounting for the 12 to 18 months of development time, the ongoing maintenance burden, the internal team needed to manage integrations, and the iterative cost of adding new payment methods as markets evolve.

Then there’s the connectivity challenge. Modern payment infrastructure isn’t just a gateway — it’s a web of acquirers, alternative payment methods (APMs), local banks, digital wallets, and fraud prevention layers. Building even a fraction of that ecosystem independently requires years of relationship development and technical work. And in high-risk verticals, the complexity multiplies further. For businesses in sectors like online gaming, forex, travel, or nutraceuticals, operating through a single acquirer relationship is a liability, not a strategy. Effective high risk payment processing demands multi-channel redundancy — routing transactions through multiple providers simultaneously so that a decline at one gateway doesn’t stop revenue in its tracks.

The White-Label Alternative: Speed, Scale, and Flexibility

White-label payment solutions have matured dramatically over the past five years. What once meant a basic branded gateway is now an enterprise-grade platform capable of handling sophisticated routing logic, fraud prevention, recurring billing, tokenization, and reconciliation — all under your own brand identity.

The economics are compelling. A white-label implementation typically costs between $10,000 and $50,000 for more advanced configurations, with ongoing licensing or transaction-based fees replacing the capital expenditure model of in-house builds. More critically, integration timelines shrink from 12–18 months to as little as a few weeks. That speed-to-market advantage is not just operationally convenient — it translates directly into earlier revenue generation and competitive positioning.

For payment service providers and fintech operators assessing their options, the best white-label payment gateway for businesses is one that balances branding flexibility, integration depth, and intelligent transaction management. The platforms worth serious consideration in 2025 — including Akurateco, Nuvei, and Ikajo International — all offer smart routing, cascading capabilities, and access to hundreds of payment connectors through a single integration point.

Orchestration: The Differentiator That Changes the Equation

What truly separates modern white-label platforms from legacy gateway models is the orchestration layer. A payments orchestration platform doesn’t simply route a transaction to a single provider — it analyzes multiple variables in real time, including cost, geography, card type, and historical approval rates, to direct each payment to the provider most likely to approve it. If that attempt fails, a cascading engine immediately reroutes through backup channels, often within the same payment attempt.

This distinction matters enormously in practice. Businesses using intelligent orchestration consistently report approval rate improvements of up to 30%, alongside significant reductions in processing costs achieved through competitive provider routing. For a company processing meaningful transaction volumes, those percentage points represent substantial revenue recovery that no in-house build, no matter how well-engineered, can match without the same multi-provider connectivity.

Orchestration also addresses one of the most persistent pain points in payment operations: reconciliation. When transactions flow through multiple providers across multiple geographies and currencies, tracking settlement becomes a significant operational burden. Advanced orchestration platforms handle automated reconciliation across all connected providers, reducing manual effort, minimizing errors, and keeping finance teams out of spreadsheet purgatory.

Security, Fraud Prevention, and Compliance

The compliance argument for in-house development often overstates the control benefit while understating the cost. Achieving and maintaining PCI DSS compliance independently requires significant investment in infrastructure, auditing, and staffing. Established white-label platforms absorb this cost across their client base, extending compliance coverage through architecture — not just contractual assurance.

Fraud prevention tells a similar story. Building a competitive fraud detection engine in-house means starting from zero on model training data, rule sets, and threat intelligence. White-label platforms with decade-long operational histories bring 50-plus years of combined expertise and continuously updated models to every client deployment. Akurateco’s fraud engine, for instance, offers over 150 customizable filters and has demonstrated fraud reduction of up to 28% for clients operating in high-risk environments — a benchmark that would take years and substantial investment to replicate independently.

Tokenization is another area where white-label solutions deliver immediate value. Rather than building vault infrastructure to store sensitive card data, merchants can rely on network-level tokenization built into the platform — enabling seamless recurring payments, automatic card updates when cards are reissued, and higher authorization rates as a direct result.

The Operational Reality: What Businesses Actually Report

The case for white-label and orchestration platforms isn’t theoretical — it’s documented in the operational transformations of businesses that have made the shift. Payment service providers that have migrated from legacy in-house systems to modern orchestration platforms consistently report three outcomes: faster onboarding of new merchants, meaningfully higher approval rates, and lower chargeback exposure.

The speed of deployment is particularly striking. Companies that previously faced months-long integration cycles for new payment provider relationships now measure onboarding in days. Platforms like Akurateco advertise new integration development timelines of around 14 days — a figure that would be essentially impossible to match with an internal engineering team managing competing product priorities.

The human capital argument is also underappreciated. Engineering talent dedicated to maintaining payment infrastructure is engineering talent not building the product that differentiates the business. In an era of tight development resources and accelerating product competition, the opportunity cost of in-house payment development is increasingly difficult to justify.

So, Which Model Actually Wins?

For the vast majority of businesses — including payment service providers, fintech operators, marketplaces, and merchants operating at any meaningful scale — white-label payment processing with a sophisticated orchestration layer represents the stronger strategic choice. The capital efficiency is clear. The time-to-market advantage is measurable. The access to global payment infrastructure, intelligent routing, and enterprise-grade fraud prevention is immediate.

Building in-house retains a legitimate use case for large enterprises with highly specific technical requirements, existing regulatory infrastructure, and the engineering depth to execute and maintain the project over a multi-year horizon. For everyone else, the build path is expensive, slow, and increasingly difficult to justify when mature orchestration platforms deliver superior transaction performance out of the box.

The payments infrastructure race is no longer about who builds the most sophisticated internal system. It’s about who routes transactions most intelligently, connects to the most relevant providers, and recovers the most revenue from every payment attempt. On those metrics, white-label orchestration has already won.